.png?width=150&height=63&name=TWRlogo-regmark_blueblack%20(1).png)

.png)

There’s been lots of talk about the differences in bank “reconciliation” between Xero and QBO. In Xero, bank reconciliation is streamlined into a single step with bank line classification, whereas in QBO, the process is more like old-school checkbook balancing. Both methods have their pros and cons and are likely to appeal to different users based on your comfort level with automation vs. manual verification. In this article, we’ll focus on the differences in the first piece – coding – and cover reconciliation in a future article.

This is the second article in a series for bookkeepers on the key differences between Xero and QuickBooks. You can read the first article here.

Your guides in this article are Rachel Barnett, founder and owner of Gentle Frog and a Top 100

ProAdvisor, who supports mostly QuickBooks clients, and Amanda Aguillard, CPA, Chief Operating Officer of Padgett and author of Xero: A Comprehensive Guide for Accountants and Bookkeepers. Rachel and Amanda have worked with hundreds of accounting professionals through their training businesses.

Coding Transactions in Xero vs. QuickBooks

Are you the type of user who wants to automate as much as possible so you can speed up your workflow? Or do you prefer to put your eyes on each transaction for the peace of mind that it brings? Comparing bank line coding in Xero and QuickBooks may give you some clues about which software is right for you, whether you’re a veteran user or just getting started. Let’s take a look at the steps involved for each software.

The Classification Process in Xero and QuickBooks

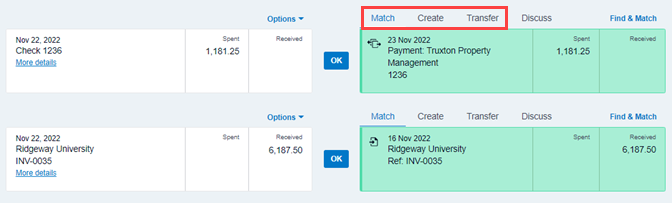

In Xero, coding a bank line creates a journal entry to the bank or credit card account. Lines are

classified in one of three ways

- Create a new entry through a spend or receive money transaction.

- Match to an outstanding bill or invoice to post a payment.

- Transfer funds between bank or credit card accounts.

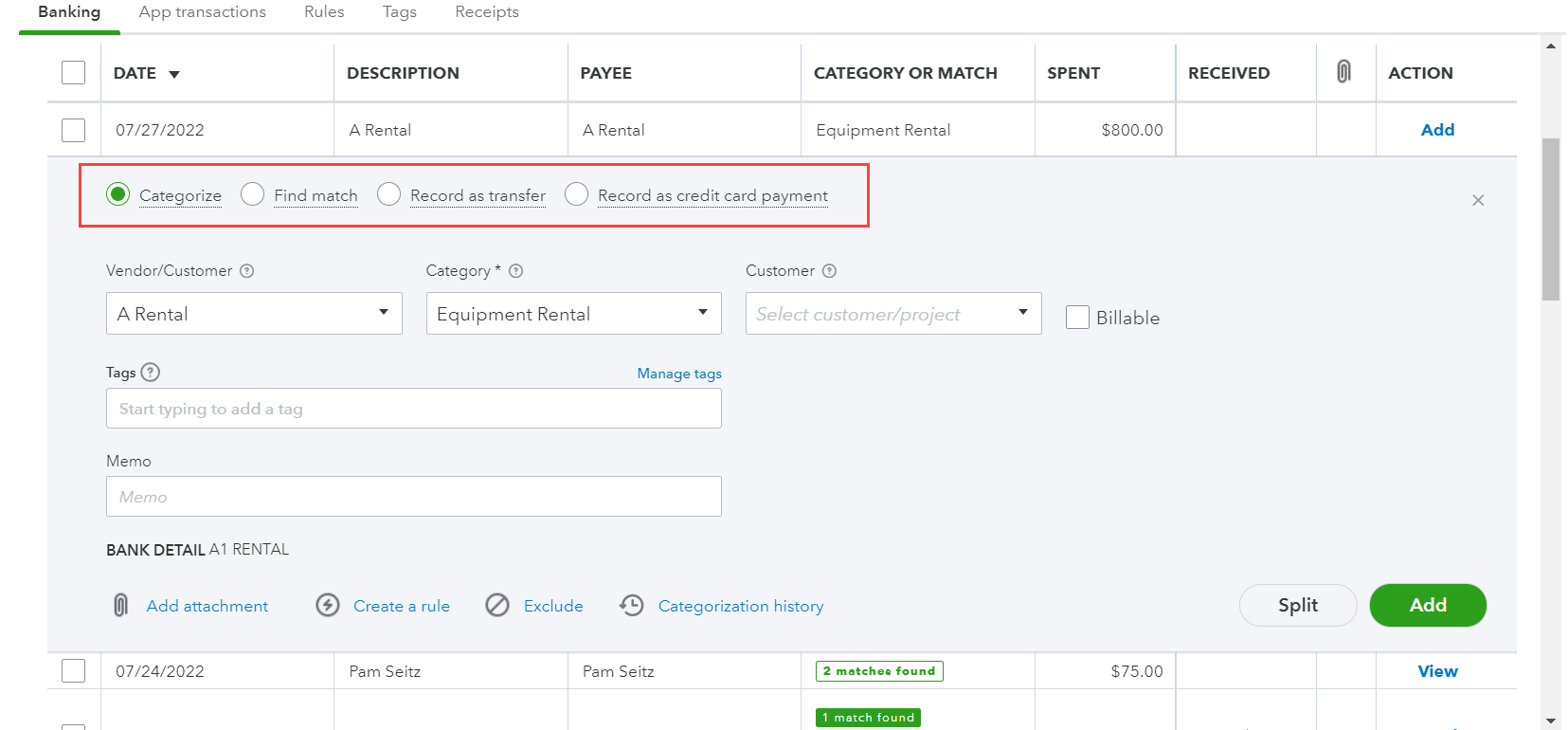

The QuickBooks expenses and deposits coding process also includes three classifications:

- Categorize - which is the same as creating a new entry in Xero.

- Find match - this allows users to match to an existing transaction that is already recorded in QuickBooks (this could be an outstanding bill or invoice as noted in the Xero classification above), OR match to a record you previously recorded in the software. Here’s an example; let’s pretend you have previously recorded a deposit in QuickBooks. Once the deposit has been downloaded from the bank into QuickBooks, you can match that information by syncing it with the information that was already in QuickBooks.

- Record as transfer - this is also the same as Xero.

- Record as credit card payment – this is a special type of transaction that reduces the balance in a credit card type account

Classification Predictions for Time Saving

During the classification process, both Xero and QuickBooks try to reduce manual data entry for their users by making suggestions about which action to take. Depending on your preferred workflow, these predictions can be incredibly useful or potentially disastrous. Let’s take a look at how each software manages predictions.

Predictions in Xero

To take advantage of predictions in Xero, Amanda notes it’s important to approach coding in a specific order:

- 1. The first coding should be done to confirm or decline Xero’s matches with existing transitions. This ensures that deposits or draws are not miscoded directly to revenue or expense accounts, which would overstate or understate income.

- 2. The next step is to code transactions using bank rules. Xero has a sophisticated query tool that makes building tailored bank rules easy. Bank rules populate within cash coding so that many bank lines can be coded automatically with just one click.

- 3. In my experience, matching and bank rules with cash coding will likely classify most transactions for typical clients, but there will always be some straggler lines, such as for paper checks, bulk deposits, or transfers. Those remaining lines should be recorded individually in the Reconcile tab of the bank account screen.

- 4. Xero may suggest coding based on prior transactions. The suggestion will show up in italics within the coding tile. (Amanda: Xero is somewhat secretive about the algorithm used for suggestions but has been open about investing in continuous improvement here.)

Amanda’s thoughts: Xero’s automation means that it has many safeguards in place to keep the user from accidentally double-entering information. Each time you accept a transaction that is downloaded from the bank, you’re relying on this automation to be accurate and can more quickly reconcile a transaction.

Predictions in QuickBooks

QuickBooks will also suggest actions to take, but Rachel’s advice is to tread carefully, especially where rules and matching are concerned. She’s helped many clients sort out disasters caused by not paying close enough attention to matching or setting up rules incorrectly. As with Xero, the QBO user will also benefit from a sequential approach:

- 1. The first step in QuickBooks is the same as in Xero: confirm the matches with existing transactions. You can easily see these in the ledger, and it’s a simple click to confirm or edit.

- 2. For coding transactions, Rachel prefers going line-by-line. However, QuickBooks also offers the ability to create rules. Where Xero automatically imports information for rules, the process is more manual in QuickBooks, which could lead to errors (the saying “garbage in, garbage out” definitely applies here!). The user needs to decide if the time saved in a manual entry is great enough that it’s worth using the rules feature. If you’re willing to answer a few questions about each transaction, using rules can make coding faster by increasing the number of matches QBO identifies for you. You can even have QBO automatically confirm the matches, saving even more time; however, Rachel advises against choosing to automatically confirm.

- 3. For all other transactions needing classification, you’ll go through the same process of choosing “Categorized,” “Matched,” or “Record as Transfer” noted above.

Rachel’s thoughts: In QuickBooks, you balance your checkbook (or credit card or loan) by looking at your entries for the month and comparing that to your statement and marking things off. This is similar to how some users may remember reconciling their checkbooks back in the day. Many bookkeepers, including me, like to have a way to double-check ourselves, and reconciling against the bank statement is how we find and fix mistakes. If that’s you, then you may appreciate the ability to manually manage coding in QBO.

Closing Advice from Rachel and Amanda

In a nutshell, the main difference is that in Xero, you reconcile AS you enter the transactions that are downloaded from the bank. In QuickBooks, you reconcile AFTER everything is entered by comparing your bank statement to the software. Neither software is more right than the other – it really comes down to your preferred workflow and preference.

Upcoming Articles on Xero and QuickBooks

Still to come from Rachel and Amanda:

Invoicing & Sales

Reports & Settings

Accounts Payable

Do you have questions about this article? Email us and let us know > info@woodard.com

Comments: